Can You Buy a Home With Student Loans? What First-Time Homebuyers Should Know

Can You Buy a Home With Student Loans? What First-Time Homebuyers Should Know

Student loans are back in the spotlight. And whether you've been following the headlines closely or just catching bits and pieces here and there, there's a good chance they've been on your mind lately.

And if you’re questioning whether you have to hit pause on your plans to buy a home, here's the thing you have to remember:

Whether you're planning to buy a home in North County San Diego or elsewhere, having student loans doesn't automatically mean buying a home has to wait.

Does Having Student Loan Debt Prevent You From Buying a Home?

One of the most common misconceptions among first-time buyers is that they have to pay off their student loans before they can qualify for a mortgage. But in most cases, that's just not true.

As an article from Redfin explains, student loans usually get evaluated the same way other debts do, like credit cards or car payments:

“Yes, you can get a mortgage with student loan debt. Lenders primarily assess your debt-to-income (DTI) ratio, which compares your monthly debt payments, including student loans, to your gross monthly income. Having student debt doesn’t automatically disqualify you if your DTI is within acceptable limits.”

So having that loan on your credit report isn't some special red flag that immediately disqualifies you.

How Mortgage Lenders Evaluate Student Loan Debt

Instead, lenders look at your overall financial situation, including your income, credit history, and more. Student loans are one piece of that puzzle, but they’re not the entire picture.

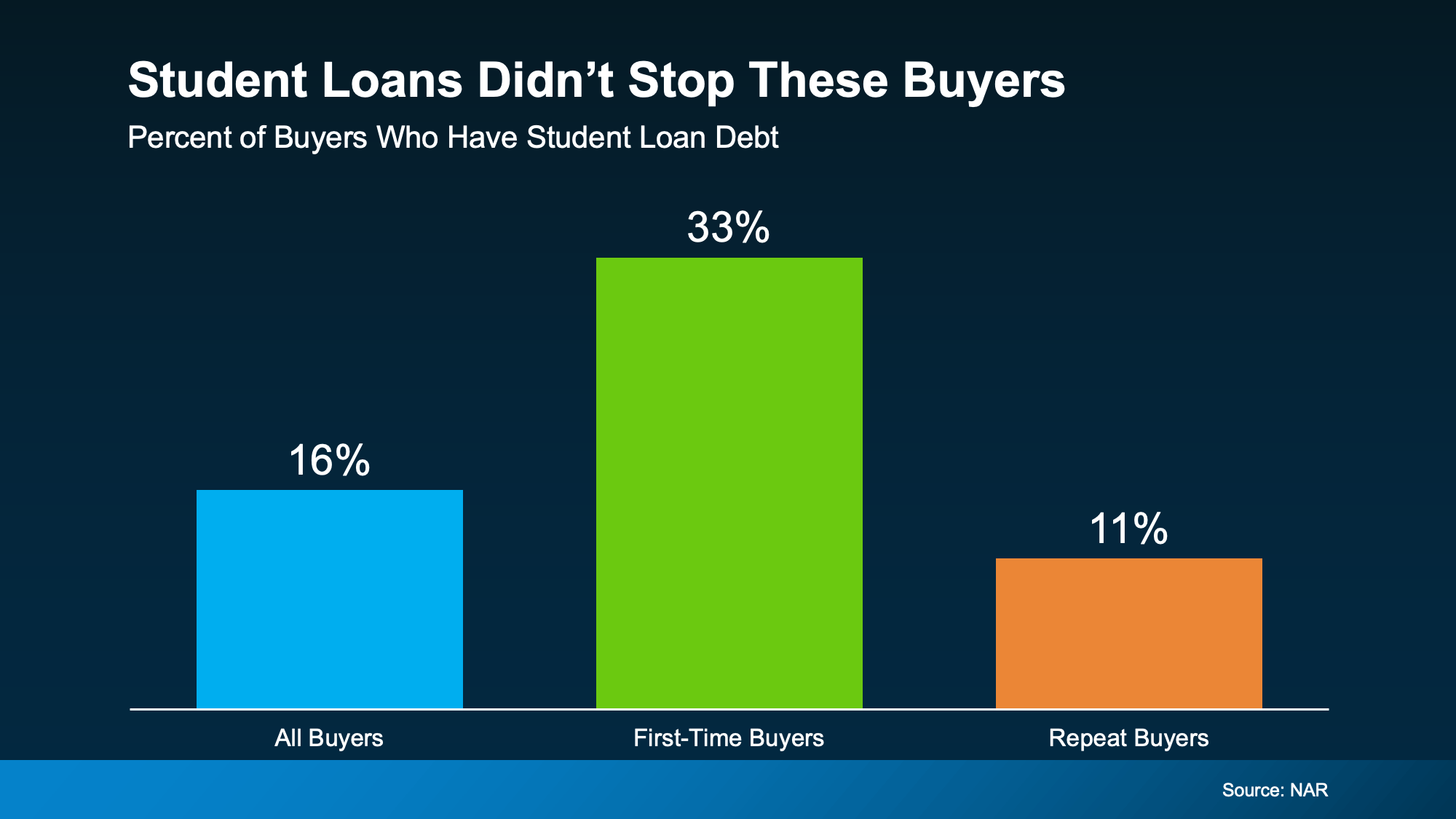

33% of First-Time Homebuyers Have Student Loan Debt

Here's a statistic from the National Association of REALTORS® (NAR): 33% of first-time homebuyers had student loan debt when they purchased their home.

That's about one out of every three first-time buyers. Among first-time homebuyers with student loan debt, the median student loan balance was $30,400.

Let that reassure you that people are buying homes with student debt every day. And carrying student loans doesn't automatically put homeownership out of reach.

Can You Qualify for a Mortgage if You Have Student Loans?

At the end of the day, here's where a lot of buyers trip themselves up. They assume the worst and never even check what they could actually qualify for. But your situation is more unique than a blanket "no."

If your income is steady and the rest of your finances are in decent shape, buying a home could be more realistic than you think. The only way to know for sure is to speak with a qualified lender who can evaluate your individual financial situation.

You may discover you're closer to buying than you think.

Bottom Line: Student Loans Don't Automatically Prevent Homeownership

Student loans don't have to be the thing standing between you and owning a home. If you've been putting off your homebuying plans because of that debt, talking with a qualified lender can help you better understand your financing options and whether you're ready to buy.

If you're planning to buy a home in North County San Diego, including Carlsbad, Oceanside, Vista, San Marcos, Escondido, or nearby communities, I'm here to help you navigate the homebuying process every step of the way.

You can also explore these helpful resources:

- Search Homes for Sale

- Find Out What Your Current Home Is Worth

- View the Latest North County San Diego Housing Market Snapshot

- Estimate Your Monthly Payment With a Mortgage Calculator

- Contact Me if you have questions about buying or selling a home in North County San Diego.

Frequently Asked Questions About Buying a Home With Student Loans

Do You Have to Pay Off Student Loans Before Buying a Home?

In many cases, you do not have to pay off your student loans before buying a home. Mortgage lenders typically consider your overall financial profile—including your income, credit history, debt-to-income (DTI) ratio, assets, employment, and existing debts—when evaluating a mortgage application. Having student loan debt does not automatically prevent you from qualifying for a mortgage, although eligibility depends on the lender's requirements and your individual financial situation.

Can You Qualify for a Mortgage if You Have Student Loan Debt?

It may be possible to qualify for a mortgage while carrying student loan debt. Mortgage lenders generally evaluate factors such as your income, credit history, debt-to-income (DTI) ratio, assets, employment, and overall financial profile. Every buyer's situation is different, so speaking with a qualified lender is the best way to understand your financing options and whether you're ready to buy.

Do Student Loans Affect Your Debt-to-Income (DTI) Ratio?

Student loan payments are generally included when mortgage lenders calculate your debt-to-income (DTI) ratio. Your DTI compares your monthly debt payments to your gross monthly income and is one of several factors lenders may consider when evaluating a mortgage application. A lower debt-to-income (DTI) ratio may strengthen your mortgage application, but mortgage qualification depends on your overall financial profile and the lender's underwriting requirements.

About Patricia Villanueva, Your North County San Diego Real Estate Agent

Patricia Villanueva is a real estate agent serving North County San Diego, including Carlsbad, Oceanside, Vista, San Marcos, Escondido, and nearby communities. Whether you're buying your first home, selling your current property, or simply exploring today's North County San Diego housing market, Patricia Villanueva is committed to providing reliable information, local market insights, and guidance throughout the real estate process.

From understanding current market trends to navigating each step of buying or selling a home, Patricia Villanueva focuses on helping clients make informed real estate decisions based on their unique goals and circumstances.

If you have questions about buying or selling a home, would like to explore homes for sale in North County San Diego, learn your home's current market value, or receive a local housing market update, contact Patricia Villanueva to get started.

Disclaimer: This article is for informational purposes only and should not be considered financial, legal, or tax advice. Mortgage qualification and financing options depend on your individual financial situation and your lender's underwriting requirements.

Categories

- All Blogs (146)

- Buyer & Seller Resources (23)

- Buyers (4)

- First-Time Buyers (34)

- Foreclosure Trends (2)

- Foreclosure Updates (2)

- Home Buying Tips (58)

- Home Improvement (1)

- Home Selling Tips (44)

- Homebuyer Tips (33)

- Homeowner Tips (20)

- Housing Market Insights (27)

- Housing Market Trends (49)

- Market Updates (26)

- Mortgage Education (14)

- Mortgage Insights (12)

- New Construction (5)

- Pricing Strategy (2)

- Real Estate Advice for Buyers (32)

- Real Estate Advice for Sellers (30)

- Real Estate Insights (21)

- Real Estate Market Updates (40)

- Renting vs. Owning (4)

- Retirement Planning (1)

- Seller Resources (15)

- Sellers (13)

- VA Home Loans (1)

Recent Posts