Why Today's Housing Market Is Different from 2008

Why Today's Housing Market Is Different from 2008

You've probably heard plenty of doom and gloom about the housing market lately. High rates. Stretched budgets. Headlines that make buying or selling sound like a terrible idea. But the data tells a very different story.

This isn't 2020 or 2021. It was never going to be. Those were the "unicorn years" – historic low mortgage rates, bidding wars on everything, homes flying off the market in days. That kind of market was a once-in-a-generation anomaly, not a baseline. So, when people compare today to that, of course it looks rough.

But compared to almost any other housing market in modern history? This one is holding up remarkably well.

Here's why today's housing market looks very different from the conditions that led to the 2008 housing crisis.

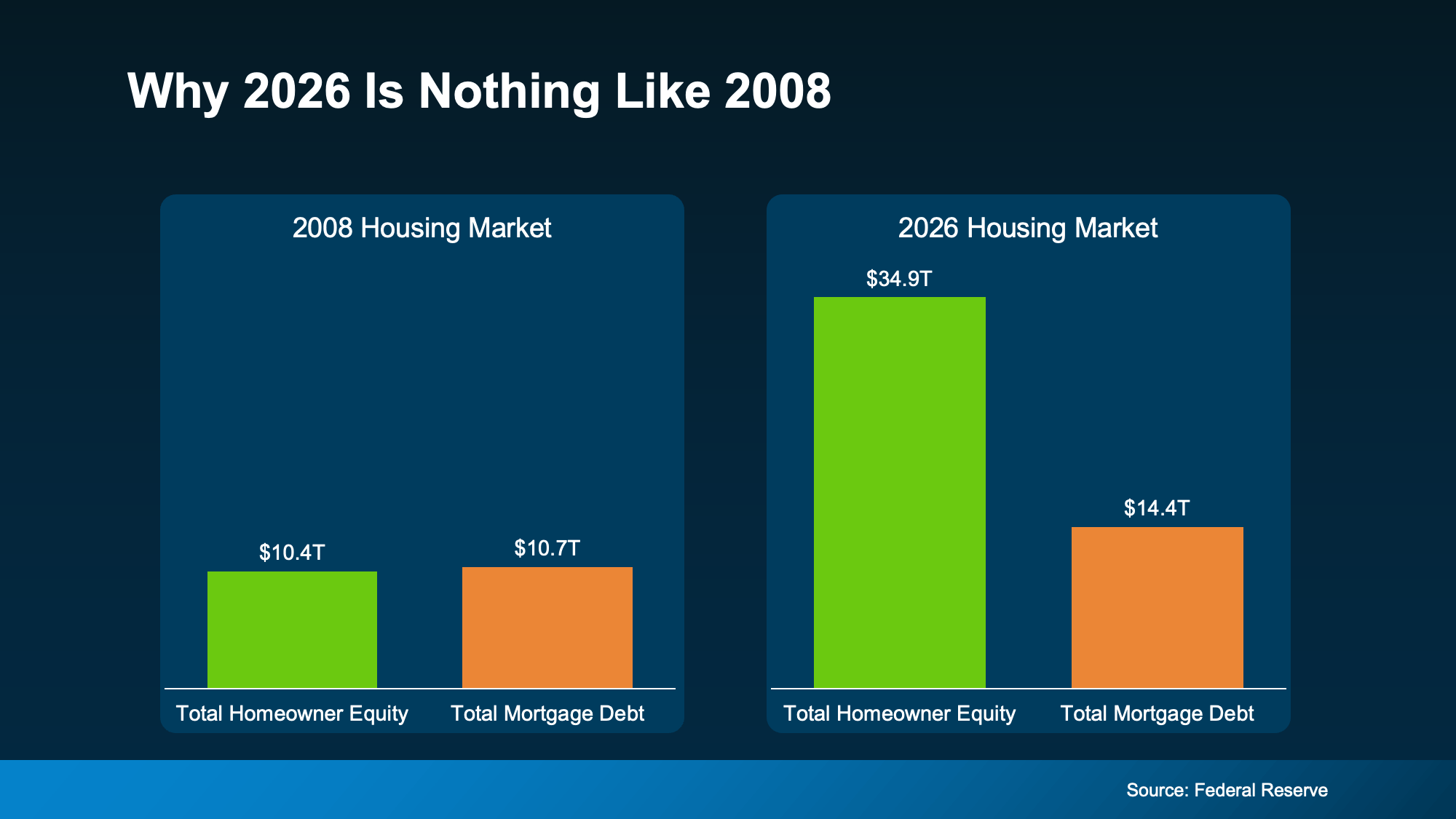

Homeowner Equity Is Much Higher Than It Was Before the 2008 Housing Crisis

One of the biggest reasons this market hasn't cracked is the financial strength of the American homeowner. According to Federal Reserve data, homeowner equity and mortgage debt were nearly identical in 2008. That meant many homeowners who experienced financial hardship had very little home equity to fall back on if they needed to sell. This was one of the factors that contributed to the severity of the housing crisis.

Today? Total homeowner equity across the country sits at $35 trillion – dwarfing total mortgage debt (see graph below):

That gap means most homeowners aren’t stretched thin or one bad month away from trouble. They own a meaningful chunk of their home and that gives them options. If they needed to sell, many could because they have a cushion. And that cushion grows over time.

- Realtor.com found that homeowners who've been in their home just 5 years have built up around $180,000 in equity on average. Stick around 6-10 years, and that jumps to over $340,000.

- Data from ATTOM and the Census shows two-thirds of homeowners either own their home outright or have more than 50% equity.

That's not a fragile market. That’s a population of homeowners who are financially positioned to sell, to stay, or to make their next move from a place of strength rather than pressure.

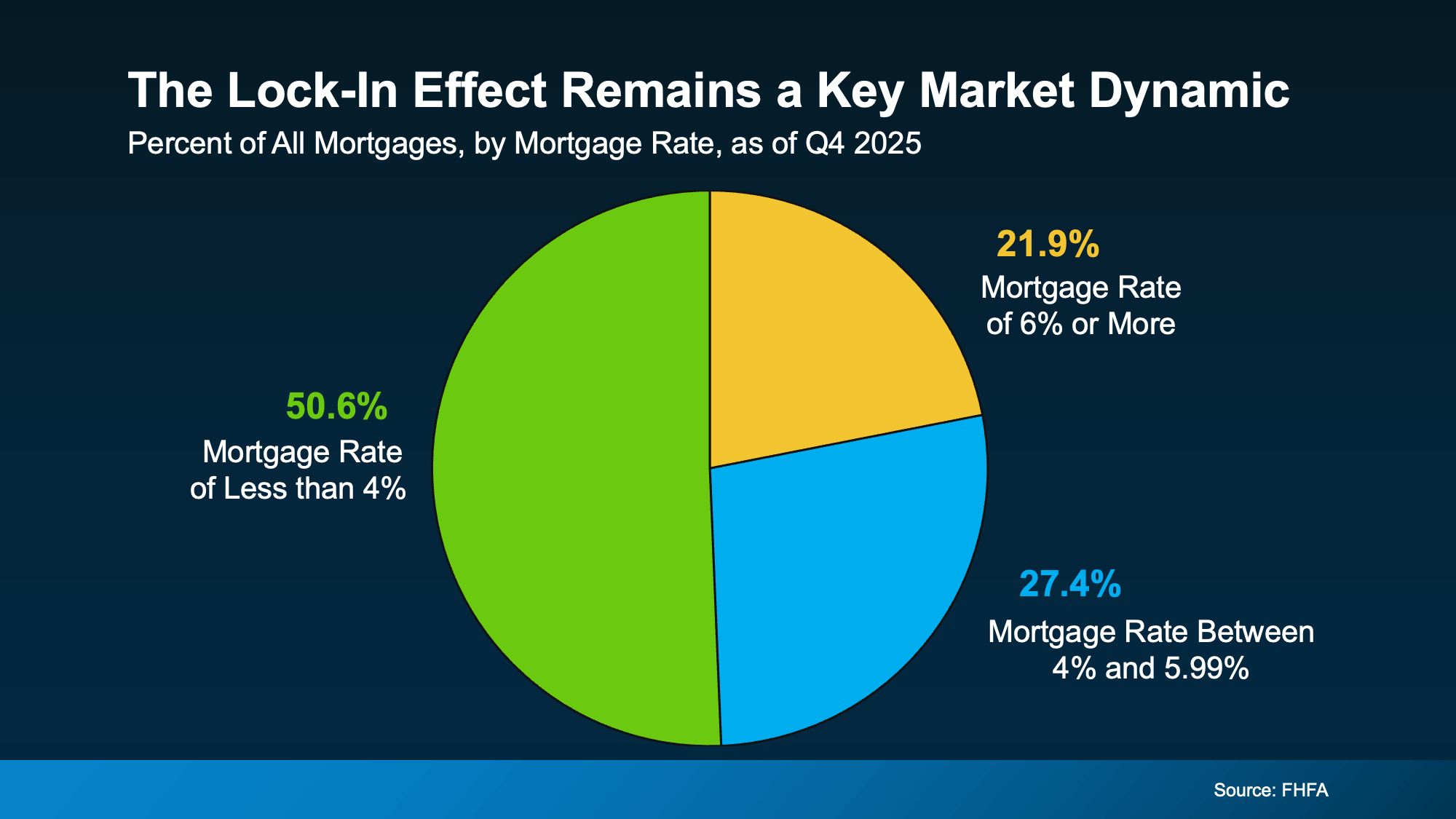

How Low Mortgage Rates and Low Foreclosures Support Today's Housing Market

At the same time, Federal Housing Finance Agency (FHFA) data shows more than half of all active mortgages still carry a rate below 4% (see graph below):

That's a big reason inventory stays tight. Those homeowners aren't in a rush to trade their rate for a higher one. They’re sitting comfortably in a strong financial position, not scrambling.

That comfort shows up in the foreclosure numbers, too. Despite a slight recent uptick, foreclosure volumes remain dramatically below historical norms, according to ATTOM. Homeowners aren't losing their homes in droves. They have equity, they have breathing room, and most have options that keep them out of financial distress.

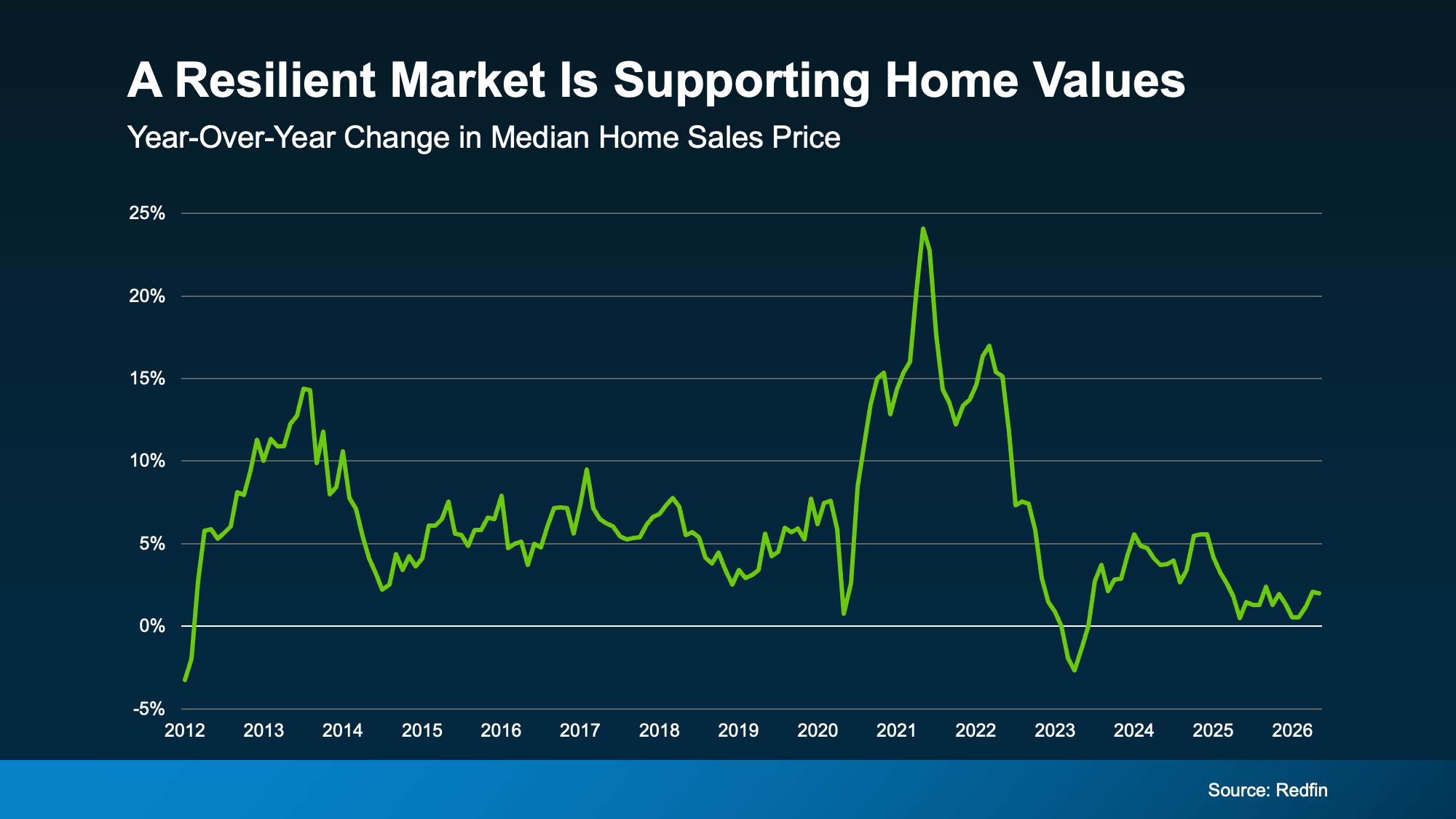

Home Prices Are Stabilizing, Not Crashing

Here’s another point on the resilience of the market. Redfin research shows home prices are still rising, but the pace has slowed, now closer to 2% year-over-year nationally (see graph below):

That slowdown is good news, as Daryl Fairweather, Chief Economist at Redfin, explains:

“We’re in the middle of a long-term housing market correction, not a housing market crash. After the pandemic-era frenzy sent prices soaring and inventory to historic lows, the market needed a reset.”

What Today's Housing Market Means for Buyers and Sellers

Today's housing market is different from the one that led to the 2008 housing crisis, and understanding those differences can help you make more informed real estate decisions. While no one can predict future housing market conditions with certainty, today's data highlights important factors—like stronger homeowner equity—that continue to shape the market.

Whether you're buying or selling a home in North County San Diego, these resources can help you make informed decisions:

- Find your home's value to see what your property may be worth in today's market.

- Search homes for sale to explore the latest listings in North County San Diego.

- View your local housing market snapshot for the latest home prices, inventory, and market trends.

- Use our mortgage calculator to estimate your monthly mortgage payment.

- Contact us if you'd like personalized guidance about buying or selling a home in North County San Diego.

Frequently Asked Questions About Today's Housing Market

How Does Today's Housing Market Compare to the 2008 Housing Crisis?

While no one can predict future housing market conditions with certainty, Federal Reserve data available in 2026 shows that today's housing market differs from the period leading up to the 2008 housing crisis in several important ways. One key difference is homeowner equity. U.S. homeowners collectively hold significantly more home equity today than they did before the 2008 housing crisis, giving many homeowners greater financial flexibility if they decide—or need—to sell.

Why Is Homeowner Equity Important in Today's Housing Market?

Homeowner equity is the difference between a home's current market value and the amount owed on the mortgage. Higher home equity may provide homeowners with greater financial flexibility if they choose to sell, refinance, or borrow against their equity. According to the Federal Reserve, U.S. homeowners collectively have substantially more home equity today than they did before the 2008 housing crisis.

Should Buyers and Sellers Wait for a Housing Market Crash?

Whether to buy or sell a home depends on your personal goals, finances, and local market conditions—not solely on national headlines. While no one can predict future housing market conditions with certainty, understanding current market data, home prices, inventory levels, and homeowner equity can help buyers and sellers make more informed real estate decisions.

About Patricia Villanueva, North County San Diego Real Estate Agent

Whether you're buying your first home, selling your current property, investing in real estate, or relocating, Patricia Villanueva helps clients make informed real estate decisions with confidence. As a North County San Diego real estate agent, Patricia Villanueva provides local market knowledge, personalized guidance, and data-driven insights to help buyers and sellers navigate every stage of the real estate process.

Serving North County San Diego, including Oceanside, Carlsbad, Vista, San Marcos, Escondido, Encinitas, Solana Beach, Del Mar, Fallbrook, Bonsall, Hidden Meadows, and nearby communities, Patricia Villanueva helps clients understand local housing market trends, determine home values, search for homes for sale, develop effective pricing strategies, negotiate confidently, and successfully navigate the buying and selling process.

Whether you're searching for homes for sale in North County San Diego, wondering how much your home is worth, exploring the North County San Diego housing market, or looking for an experienced North County San Diego real estate agent, Patricia Villanueva is committed to providing honest advice, responsive communication, and exceptional service tailored to your real estate goals.

Ready to get started? Contact Patricia Villanueva today to discuss your real estate goals or explore the helpful resources available on this website, including Home Search, Home Value, Market Snapshots, and the Mortgage Calculator.

Disclaimer: The content on this website is provided for general informational and educational purposes only. Real estate markets, home values, mortgage rates, and housing trends are subject to change and may vary by location. Information is believed to be accurate at the time of publication but is not guaranteed. This content should not be considered financial, legal, tax, or investment advice. Readers should consult qualified professionals regarding their individual circumstances before making any real estate or financial decisions.

Categories

- All Blogs (144)

- Buyer & Seller Resources (22)

- Buyers (3)

- First-Time Buyers (32)

- Foreclosure Trends (2)

- Foreclosure Updates (2)

- Home Buying Tips (57)

- Home Improvement (1)

- Home Selling Tips (43)

- Homebuyer Tips (31)

- Homeowner Tips (19)

- Housing Market Insights (27)

- Housing Market Trends (49)

- Market Updates (26)

- Mortgage Education (14)

- Mortgage Insights (12)

- New Construction (5)

- Pricing Strategy (2)

- Real Estate Advice for Buyers (30)

- Real Estate Advice for Sellers (29)

- Real Estate Insights (21)

- Real Estate Market Updates (40)

- Renting vs. Owning (4)

- Retirement Planning (1)

- Seller Resources (15)

- Sellers (13)

- VA Home Loans (1)

Recent Posts